Tax Brackets: A Simple Guide To Understanding Your Taxes And Saving More

Ever wonder why your paycheck seems smaller than expected? Or maybe you've heard about "tax brackets" and have no idea what they mean? Don't worry, you're not alone. Tax brackets are one of those financial terms that sound super complicated but are actually pretty easy to understand once you break them down. Whether you're a working professional or just starting your career, knowing how tax brackets work can help you save more money and make smarter financial decisions.

Let’s face it, taxes can feel like a mystery, especially when you hear terms like "federal income tax" or "progressive tax system." But here's the thing—tax brackets are designed to ensure fairness in the tax system. They’re basically ranges of income that are taxed at different rates, and understanding them can help you figure out how much you owe and how to plan for the future.

Think of tax brackets as a ladder. The more you earn, the higher you climb, but each step—or bracket—is taxed differently. This guide will break it all down for you, so you can stop stressing about taxes and start focusing on what matters most—your financial goals.

Read also:Lady Louise Windsor Growing Up In The Spotlight

What Are Tax Brackets, Really?

Tax brackets are basically the income ranges that determine how much tax you pay on each portion of your income. In the U.S., we have a progressive tax system, which means the more money you make, the higher the tax rate you pay on certain portions of your income. But here's the kicker—it doesn’t mean you pay the same rate on all your income. Let me explain.

Imagine your income is divided into chunks. Each chunk falls into a specific tax bracket, and each bracket has its own tax rate. For example, if you earn $50,000 a year, the first chunk of your income might be taxed at 10%, the next chunk at 12%, and so on. It's like filling up buckets with water—the first bucket gets filled at a lower rate, and as you move up, the buckets get filled at higher rates.

Here’s a quick example:

- Income up to $10,275 is taxed at 10%.

- Income between $10,276 and $41,775 is taxed at 12%.

- Income over $41,776 is taxed at 22%.

So, if you make $50,000, you won’t pay 22% on all of it. Instead, you’ll pay the lower rates on the first chunks of your income and only the higher rate on the part that falls into the 22% bracket. Makes sense, right?

How Tax Brackets Work in the Real World

Now that you know what tax brackets are, let’s dive into how they work in real life. The U.S. tax system uses marginal tax rates, which means only the portion of your income that falls into a higher bracket gets taxed at that rate. This is important because it prevents people from being penalized for earning more money.

Let’s break it down with another example. Say you’re single and your taxable income is $60,000. Here’s how the tax brackets would apply:

Read also:Why Were Adam West And Glen Campbell Left Out Of The Oscars In Memoriam Tribute

- First $10,275 is taxed at 10% = $1,027.50

- Next $31,500 ($41,775 - $10,275) is taxed at 12% = $3,780

- Remaining $18,225 ($60,000 - $41,775) is taxed at 22% = $4,009.50

Add it all up, and your total tax bill would be around $8,817. But here’s the key point—your effective tax rate (the actual percentage of your income you pay in taxes) would be much lower than the highest bracket you fall into. In this case, it would be about 14.7%.

Why Understanding Tax Brackets Matters

Knowing your tax bracket can help you make better financial decisions. For instance, if you’re close to moving into a higher bracket, you might consider strategies to reduce your taxable income, like contributing more to a retirement account or taking advantage of tax credits. It’s all about optimizing your money to keep more in your pocket.

Plus, understanding tax brackets can help you plan for the future. If you’re thinking about switching jobs or starting a business, knowing how taxes work can help you estimate your potential tax liability and make informed decisions.

Common Misconceptions About Tax Brackets

There are a lot of myths floating around about tax brackets, and it’s time to set the record straight. One of the biggest misconceptions is that moving into a higher tax bracket will leave you worse off. That’s just not true. Remember, only the portion of your income that falls into the higher bracket gets taxed at the higher rate. The rest of your income is still taxed at the lower rates.

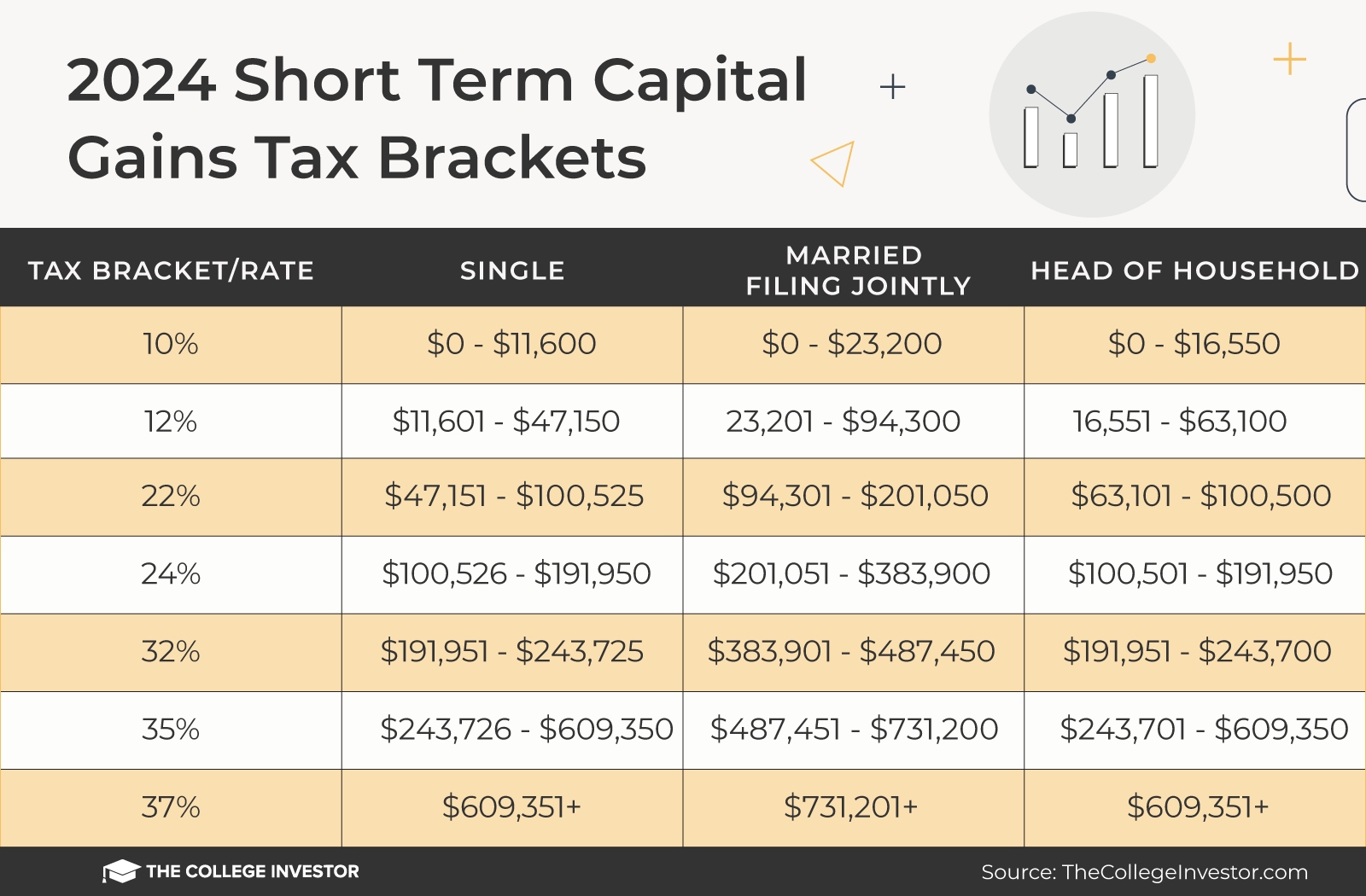

Another myth is that tax brackets are the same for everyone. In reality, tax brackets vary based on your filing status—whether you’re single, married filing jointly, or head of household. Each status has its own set of brackets, so it’s important to know which one applies to you.

Breaking Down Filing Statuses

Here’s a quick rundown of the different filing statuses and how they affect your tax brackets:

- Single: This is the default status for most taxpayers. It applies if you’re unmarried and don’t qualify for any other status.

- Married Filing Jointly: If you’re married and file a joint return, your tax brackets will be higher than if you were single. This is because the IRS assumes two people in a household can afford to pay more taxes.

- Head of Household: This status is for single taxpayers who support a dependent, like a child. It offers more favorable tax brackets than the single status.

Understanding your filing status is crucial because it determines which tax brackets apply to you. Make sure you choose the right one when filing your taxes to avoid any surprises.

How to Calculate Your Tax Bracket

Calculating your tax bracket is easier than you think. All you need to do is look at your taxable income and compare it to the current tax brackets. The IRS updates these brackets every year to account for inflation, so it’s important to check the latest figures.

Here’s a step-by-step guide to calculating your tax bracket:

- Determine your filing status (single, married filing jointly, etc.).

- Find the latest tax brackets for your filing status.

- Compare your taxable income to the brackets to see which one you fall into.

For example, if you’re single and your taxable income is $50,000, you’d fall into the 22% tax bracket. But again, only the portion of your income above $41,775 would be taxed at that rate.

Tools to Help You Calculate Your Tax Bracket

If you’re not a math whiz, don’t worry. There are plenty of online tools and calculators that can help you figure out your tax bracket. Just enter your income and filing status, and the tool will do the rest. Some popular options include TurboTax, H&R Block, and the IRS’s own tax calculator.

Strategies to Lower Your Tax Bracket

Now that you know how tax brackets work, let’s talk about how to lower yours. There are several strategies you can use to reduce your taxable income and potentially move into a lower bracket:

- Contribute to Retirement Accounts: Contributions to traditional IRAs and 401(k)s are tax-deductible, which means they reduce your taxable income.

- Take Advantage of Tax Credits: Credits like the Earned Income Tax Credit (EITC) or Child Tax Credit can lower your tax bill and potentially move you into a lower bracket.

- Itemize Deductions: If you have a lot of expenses like mortgage interest or medical bills, itemizing your deductions can help reduce your taxable income.

These strategies can save you hundreds—or even thousands—of dollars in taxes. The key is to plan ahead and make the most of the tax breaks available to you.

The Impact of Tax Brackets on Your Financial Plan

Tax brackets play a big role in your overall financial plan. They affect everything from how much you save for retirement to how much you invest in stocks. By understanding your tax bracket, you can make smarter decisions about where to put your money and how to minimize your tax liability.

For example, if you’re in a high tax bracket, you might want to consider tax-efficient investments like municipal bonds or index funds. On the other hand, if you’re in a lower bracket, you might be able to afford riskier investments that offer higher returns.

Long-Term Planning with Tax Brackets

When it comes to long-term planning, tax brackets are a key consideration. If you’re planning for retirement, for instance, you’ll want to think about how your tax bracket will change over time. Will you be in a higher or lower bracket when you start withdrawing from your retirement accounts? These are important questions to ask as you build your financial plan.

Understanding Tax Brackets for Small Business Owners

If you’re a small business owner, tax brackets are especially important. Depending on your business structure, your income might be taxed differently. For example, if you’re a sole proprietor, your business income is added to your personal income and taxed according to the same brackets. But if you’re incorporated, your business might be subject to a separate corporate tax rate.

Here are a few tips for small business owners:

- Keep detailed records of your income and expenses to ensure accurate tax reporting.

- Consider hiring a tax professional to help you navigate the complexities of business taxes.

- Explore deductions and credits specifically designed for small businesses, like the Self-Employment Health Insurance Deduction.

Tax Planning for Freelancers and Contractors

Freelancers and contractors also need to be mindful of tax brackets. Since you’re responsible for paying your own taxes, it’s important to set aside enough money throughout the year to cover your tax liability. One common mistake freelancers make is underestimating their tax bracket, which can lead to a nasty surprise at tax time.

Final Thoughts: Mastering Your Tax Brackets

Tax brackets might seem intimidating at first, but they’re actually pretty straightforward once you understand how they work. By knowing your tax bracket, you can make better financial decisions, save more money, and plan for the future with confidence.

So, what’s next? Start by calculating your current tax bracket and exploring strategies to reduce your taxable income. Whether you’re a working professional, small business owner, or freelancer, understanding tax brackets is a key step toward financial success.

And remember, if you ever feel overwhelmed, don’t hesitate to reach out to a tax professional. They can help you navigate the complexities of the tax system and ensure you’re making the most of your money. Now go out there and master your taxes!

Table of Contents

- What Are Tax Brackets, Really?

- How Tax Brackets Work in the Real World

- Common Misconceptions About Tax Brackets

- How to Calculate Your Tax Bracket

- Strategies to Lower Your Tax Bracket

- The Impact of Tax Brackets on Your Financial Plan

- Understanding Tax Brackets for Small Business Owners

- Tax Planning for Freelancers and Contractors

- Final Thoughts: Mastering Your Tax Brackets

Article Recommendations